An In-Depth Look at Wall Street's Latest Phenomenon: SPACs

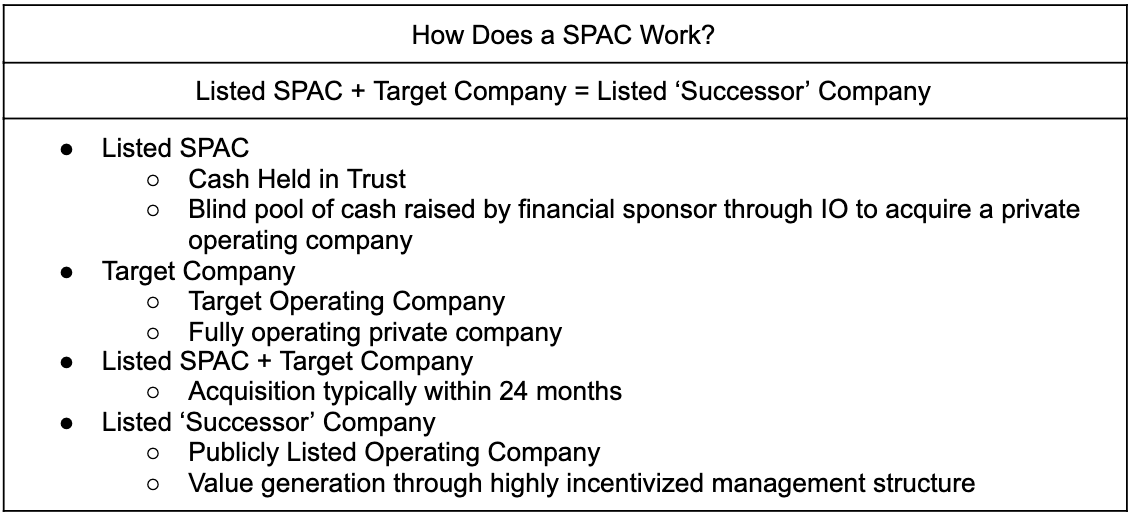

Over the course of the pandemic, methods for companies going public other than traditional IPOs have expanded to include using SPACs. SPACs, otherwise known as special purpose acquisition companies or blank check companies, are corporate entities created without any specific operations and are formed for only one purpose: raise capital through its own initial public offering to then acquire a non-public company which would then bring that acquisition to the public capital markets. They are known as blank check companies since investors do not know exactly what their specific input of capital will be used for and usually trade at a standard $10 per share in the stock market. If the merger between the SPAC and the acquired company is successful within an approximate time period of two years, the investors can then receive their return on investment. Otherwise, the SPAC is liquidated and distributed accordingly to the investors.

SPAC deals, like any other financial transaction, have definite positive and negative aspects. Many of the positive aspects are related to the removal of some regulatory restrictions that makes the process smoother. However, since SPACs are essentially cash vehicles with very restrictive time limits to acquire a company, they may encounter specific potential partners that have the common characteristic of needing cash. This may lead to a narrow demographic of target companies which then leads to further problems.

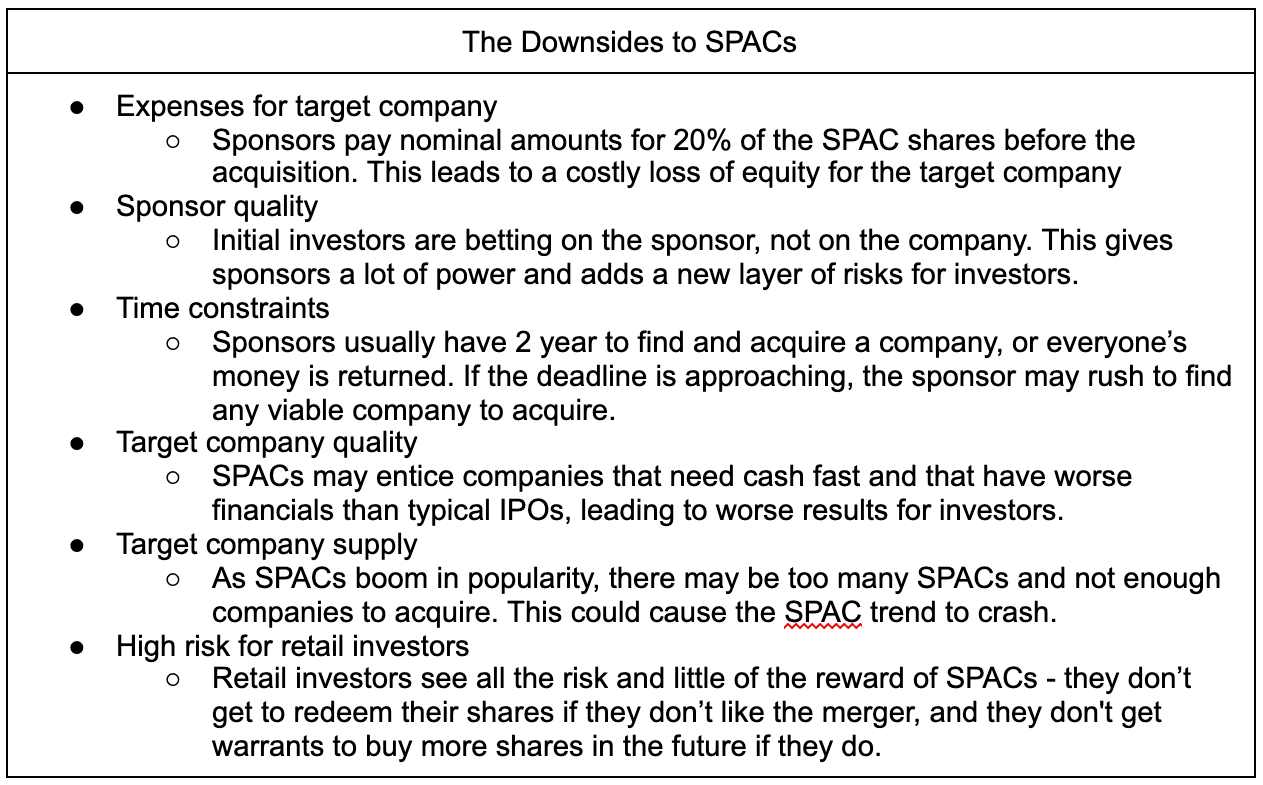

The Downsides to SPACs

- Expenses for target company

- Sponsors pay nominal amounts for 20% of the SPAC shares before the acquisition. This leads to a costly loss of equity for the target company

- Sponsor quality

- Initial investors are betting on the sponsor, not on the company. This gives sponsors a lot of power and adds a new layer of risks for investors.

- Time constraints

- Sponsors usually have 2 year to find and acquire a company, or everyone’s money is returned. If the deadline is approaching, the sponsor may rush to find any viable company to acquire.

- Target company quality

- SPACs may entice companies that need cash fast and that have worse financials than typical IPOs, leading to worse results for investors.

- Target company supply

- As SPACs boom in popularity, there may be too many SPACs and not enough companies to acquire. This could cause the SPAC trend to crash.

- High risk for retail investors

- Retail investors see all the risk and little of the reward of SPACs - they don’t get to redeem their shares if they don’t like the merger, and they don't get warrants to buy more shares in the future if they do.

2020 was a prominent year for SPACs with there being four times as many of these entities set up (242) compared to 2019 with the average size of the SPAC increasing to $335 million. Thus, an interesting question to look at is the rationale for such an increase in SPACs in the pandemic which then leads to estimating future projections of SPACs in a global perspective. One high-profile example of SPACs during this pandemic has been seen in the activity of venture capitalist Chamath Palihapitiya. He has been notorious for “serial SPAC-founding” like he has done with Virgin Galactic and the 13 other SPAC deals he has been involved with. However, even with the rapidly growing popularity of SPACs, it is a definite possibility that the SPAC market can contract, albeit in a limited fashion. The coronavirus pandemic created an IPO market with extreme volatility and unpredictable nature which lessened the appeal of the IPO process. Generally, the IPO process is preferred since it is much more direct for the company to go to the market and has been a traditional approach of taking companies public. But with market volatility, the SPAC method is advantageous by just having two negotiators between the company and the SPAC itself instead of a company and multiple investors as done in the IPO. Also, terms are agreed to at an earlier state of the process for the SPAC which creates a better established foundation for the rest of negotiations. Also, SPACs have smaller timelines to complete deals since there are no company operations other than finding a suitable partner company for acquisition.

Thus, while the SPAC market will contract post-pandemic with market volatility expected to decrease during such a time period, it will not return to its initial pre-pandemic condition due to its exposure to the public as a very versatile method of taking companies public. The SPAC method’s public exposure has led to international attention and other global regions trying to participate. This could be seen by Great Britain recently changing their listing rules for the sole purpose of being more receptive to “hot” markets like technology and SPACs to maintain its competitive edge against other prime European financial centres. Therefore, the SPAC market will be still much more active relative to pre-pandemic times, yet not as much as it is at the moment.

There are many different opinions about how SPACs will continue to do in the future. For example, there are some analysts who say that the rise of SPACs have stopped for the first time since the beginning of the pandemic. These arguments are supported by recent developments of many SPACs trading at prices below the standard $10 and a relevant benchmark for SPACs falling into bearish market territory. Such proponents of this perspective have been seen in the news like Palihapitiya’s sale of more than $213 million worth of Virgin Galactic stock.Others discuss this trend as a bubble that may be close to bursting and thus, causing investors to lose much of their investment. On the other hand, with there being an appetite for growth stocks, some analysts are still optimistic about SPACs as efficient methods for going public because many of these growth-stock potential companies now have an avenue to reach the public capital markets. With these opinions in mind, this article thus concludes that there are relative causes which will cause a SPAC market contraction, yet not enough to outweigh the benefits of going public via SPAC. SPACs will become more viable and prevalent in a global sense and change based on variables such as current volatility of the market.