Entering the New Era of ESG: The Current State of the Canadian ESG Reporting Environment

Environmental, Social and Governance, also known as ESG, is a rising topic in today’s world. The importance of carbon footprints, sustainability, human rights and the organizational structure of a firm are more important than ever to ensure the success of a firm in the long term. New regulations have been observed by governments to address the needs of stakeholders and have changed the reporting landscape for companies across borders. Readers may find this introduction to ESG in Canada that addresses its importance, particularly in the environmental aspect concerning greenhouse gas emissions (GHG) helpful as they navigate the ethical and social responsibility behind ESG reporting.

Why is ESG reporting important?

As defined by the Green Business Bureau, ESG reporting is the disclosure of data covering business operations related to the environmental, social, and governance aspects of a business.

There are 4 main reasons as to why ESG reporting is important:

Creates transparency

ESG looks at regulation as a means for transparency for a variety of stakeholders such as investors, employees and customers. Transparency can not only push for solutions for global issues like climate change and equality, but also encourages accountability through disclosure.

Attracts investors and financing

Investors and lenders are increasingly interested in using ESG reports to assess a firm’s risk exposure. In fact, according to PwC, asset managers globally are expected to increase their ESG-related assets under management to US$33.9tn by 2026, from US$18.4tn in 2021. (Stanton 2022) This signals the increasing demand among investors for transparency and disclosure of ESG practices.

Meets stakeholder demand

According to an Ipsos poll conducted in 2021, two thirds of Canadians (65%) say that ESG factors play an important role in helping them to decide their investment strategies and purchase decisions. This percentage was most prominent among Gen Z and millennials within the ages of 18-34 at 71%, compared to their 35-54 year-old counterparts at 65% in agreement. According to Morningstar, U.S. millennials already played a significant role in ESG investing, having contributed $51.1 billion to sustainable funds in 2020 compared with less than $5 billion in 2015. The rising demand from Canadians and Americans for ESG reporting aligns with their goals to align investments with their values. As such, transparency, disclosure and ESG reporting standards are increasingly important in the investment landscape.

Response to regulation change

As mentioned previously, many proposals and draft guidelines have been released by various government bodies pushing towards mandatory reporting on ESG and climate-related risks. These actions taken by government institutions point towards the upcoming new disclosure guidelines, which may be a big step for entities compared to the non-mandatory reporting that had been in place in previous years. These changes highlight the importance for entities to stay up to date on developing standards.

What are the positive effects of ESG on the environment and society?

Environment: Improvements in attitude towards sustainable development and climate change

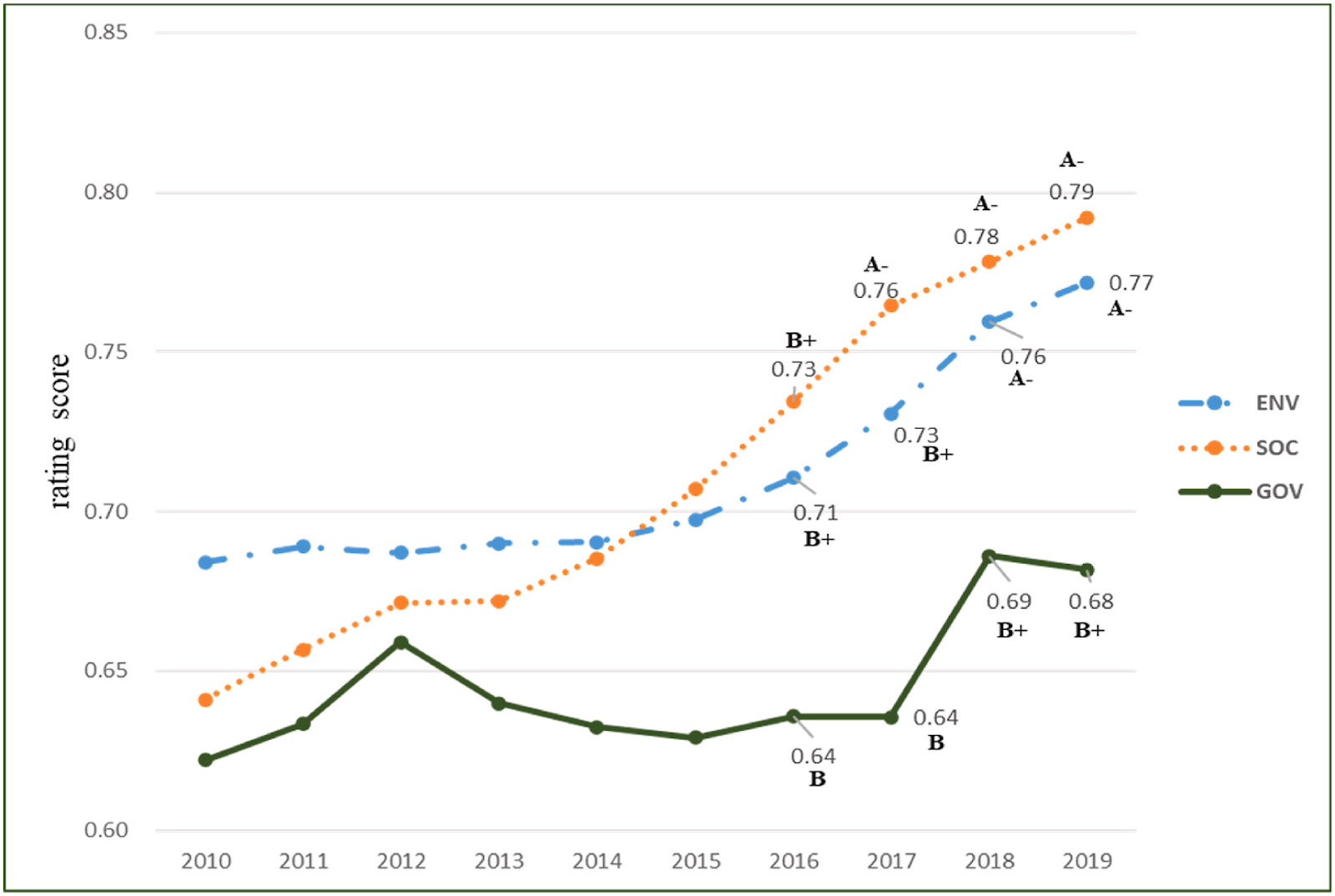

According to the scholarly article Impacts on the ESG and financial performances of companies in the manufacturing industry based on the climate change related risks written by Chen et al. in 2022, they concluded that the increasing risk of climate change crises has assisted government organizations in achieving the United Nations sustainable development and Paris Agreement goals.

Based on their research, following the natural disasters between 2017 and 2020, manufacturing companies increased spending in ESG factors and the implementation of ESG activities in the company in 2018-2019. Consequently, their environmental, social and governance ratings increased as firms adopted appropriate climate risk management and increased transparency as their risk salience increased (Huang et al). As a result, the improved ratings also reflected the attitudes of firms towards achieving sustainable development and reducing emissions.

Source: Chen et al. 2022

Social: Working conditions and community change

The “S” in ESG often overlaps with the environmental and governance factors. For instance, pollution is both a workplace and a wider societal issue, and coal can give miners black lung disease, apart from contributing to carbon emissions. (Muller 2019) The overlaps mean that it is rather difficult and not as popular to measure compared to the environmental factor. The increasing awareness of the social factor in ESGs has also led to change within firms, as public opinion now holds companies responsible for their attitudes towards human rights issues. In 2012, a Bangladesh factory collapse revealed the unsafe working conditions of the workers. Joe Fresh was among the clothing labels who had clothes made, and customers horrified by the incident threatened to boycott the brand unless changes were made. This matter signals the importance of addressing human rights and labour conditions of workers for various entities, as well as improvements thanks to the prevalence of social media today.

A Canadian Example: CN Rail

An example of a Canadian company taking steps in ESG is Canadian National Railway, also known as CN. As a leading North American transportation and logistics company, it spans from the North to Central America offering integrated rail and other transportation services, including trucking, warehousing and distribution. They have published their Carbon Disclosure Project (CDP) for years, addressing the TCFD framework and GHG emissions goals based on Scope 1, 2 and 3.

In order to address the environmental impact of their emissions from their transportation services, CN partnered with Progress Rail and the Renewable Energy Group (REG) to test high-level renewable fuel blends, including biodiesel and renewable diesel. In addition, their strategy to make the transition to low-carbon usage involves fleet renewals, innovative technologies, big data analytics, operating practices, and the greater use of renewable fuels. With appropriate changes to their fleet and operations, they successfully met their 5-year emissions target for Scope 1 emissions from 2017-2022 and their year-on-year targets.

Their social impact involves a reforestation program in communities near their rail networks. The EcoConnexions From the Ground Up is a reforestation program created by CN in 2012 that promotes the planting of trees near the CN rail network. The EcoConnexions program is not only a community program and an employee engagement program, but also works as a partnership program with CN customers and suppliers who demonstrate dedication to sustainability initiatives. As of 2012, they have planted more than 2.3 million trees combined in Canada and the U.S and trained over 800 employees in their EcoChampion initiative. Their activity not only spans the environmental impact, but also the social aspect concerning their employees and their local community.

What is the current ESG reporting environment in Canada?

In previous years, there were no legal requirements for companies to make any ESG disclosures in Canada. Canada in recent years has taken a step forward on this front due to ESG’s increasing prevalence to require federally regulated financial institutions to publish ESG disclosures and assess collected client information on climate risks and emissions ( Government of Canada).

This year, the Office of the Superintendent of Financial Institutions (OSFI) has issued Draft Guideline B-15 Climate Risk Management outlining guidelines for federally regulated financial institutions and their management of climate-related risks. In particular, the draft is separated into 2 chapters: Governance and Risk Management Expectations, and Climate Related Financial Disclosure. Included are a number of details regarding expectations, including the implementation of tools to measure climate-related risks, climate scenario analyses and ensuring capital and liquidity adequacy. The guidelines include expectations based on the Task Force on Climate-Related Financial Disclosures (TCFD) recommendations and the ISSB’s Draft on Climate-Related Disclosures (IFRS S2) that was also issued this year for public comment.

A look outside: What measures have been adopted in the United States?

In 2022, the SEC released the proposal The Enhancement and Standardization of Climate-Related Disclosures for Investors that would require “require information about a registrant’s climate-related risks that are reasonably likely to have a material impact on its business, results of operations, or financial condition.” The proposal does reference the TCFD framework, and also suggests measuring GHG emissions to determine the exposure to climate-related risks. In particular, other rules listed would require entities to disclose:

- direct greenhouse gas (GHG) emissions (Scope 1);

- indirect GHG emissions from purchased electricity and other forms of energy (Scope 2); and

- indirect emissions from upstream and downstream activities in a company’s value chain (Scope 3).

Of note is a proposed rule regarding the disclosure of carbon offsets or renewable energy credits if used. These Renewable Energy Credits or Certificates (RECs) are defined using the EPA’s commonly used definition, to mean a credit or certificate representing each purchased megawatt-hour (1 MWh or 1000 kilowatt-hours) of renewable electricity generated and delivered to a registrant’s power grid. As stated by the SEC:

“If, as part of its net emissions reduction strategy, a registrant uses carbon offsets or renewable energy credits or certificates (“RECs”), the proposed rules would require it to disclose the role that carbon offsets or RECs play in the registrant’s climate-related business strategy.”

Canadian entities with business in the U.S may also be impacted by the proposal. The SEC included a request for comment on whether Canadian issuers eligible to reporting under the Multijurisdictional Disclosure System (MJDS) should be exempt, which opens the door to the possibility that Canadian companies listed on a U.S. exchange may ultimately be subject to the proposed SEC rule.

It is important for Canadian entities to follow news regarding ESG standards in the U.S since there exists strong economic and political ties between the two countries that may also affect Canadian climate-related risk disclosures. This can be seen when the CSA referenced the release of the SEC’s proposal in their statement to review the Proposed National Instrument 51-107 Disclosure of Climate-related Matters (NI 51-107) for alignment with the ISSB.

The current issue in the ESG reporting landscape: a lack of overall quality

According to a study by Amel-Zadeh et al., “little is known about how investors use ESG information” (p. 93). In fact, studies show that issues in ESG reporting today include a lack of relevance and materiality, a lack of accuracy for evaluating a firm’s actual sustainability performance, lack of reliability in the ESG self-assessment by companies and a lack of comparability.

- Materiality

Although companies are aware of the importance of ESG reporting and have increased their disclosure, the information provided is typically generalised, creating irrelevant information towards investment decision making. A potential explanation may be that ESG data is a “tick the box” approach by entities due to the rise in specialist rating agencies (SRAs) evaluating sustainability performance, as well as the general demand increase for ESG. According to study by Kotsantonis et al., half of the fifty companies in the Fortune 500 in their study reported having a health and safety policy, and 15% disclosed their lost time incident rates and workplace fatalities. The small percentage of disclosure is significant since the SASB framework considered employee health and safety as a material ESG issue (p. 50).

2. Accuracy

Accuracy in evaluating a firm’s ESG performance may not be of good quality. Kotsantonis et al. further proved that the lack of alignment in reporting frameworks increased the complexity and resources needed to create an ESG report. As a result, the information disclosed may become increasingly inaccurate as the companies might either provide information that is irrelevant or try to avoid disclosure.

3. Reliability

Another issue is reliability in company reporting. Given that companies release their own ESG reports, those with poor results may use language that is imprecise but optimistic in an attempt to mislead investors (Melloni et al. 2017). This can be misleading as the firm attempts to generate a positive outlook on their disclosure. In order to reduce the risk of whitewashing, “many of the global SRAs, including MSCI, RepRisk and Refinitiv, commonly aggregate ESG data only from external, public data sources. The SRAs collect external data via sources including audited financial statements and annual reports of the disclosing companies, media information, companies’ websites or other publicly accessible data sources”. (Jonsdottir et al. 2022)

4. Comparability

While examining a survey of 652 investment professionals, the greatest challenge mentioned by investors in utilising ESG data as a base for investment decisions stemmed from a lack of cross-company comparability. (Amel-Zadeh and Serafeim 2018) The lack of comparability may potentially be due to the increasing amount of disclosure in ESG reporting, making it difficult for investors to determine the value of ESG outcomes. (Christensen et al. 2022)

These 4 elements are further proven in the interviews with institutional investors and company employees conducted by Jonsdottir et al., where they echo issues like the lack of comparability, and introduce a new issue: greenwashing.

ESG Reporting Issue: Greenwashing

The origins of the word “greenwashing” stem from American environmentalist Jay Westervelt’s hotel visit in the 1980s where he noticed signs asking guests to reuse their towels in order to “save the environment.” Over the period of his stay, he noted a significant amount of wastage and no obvious effort towards sustainability. As a result, he felt that the hotel was trying to cut costs by reducing the frequency of washing towels but marketing the action as eco-friendly behaviour. Today’s definition is relatively similar, and is determined as when an entity attempts to hide under the cover of being environmentally-friendly, may it be using ESG disclosures or the use of vocabulary such as “green” or “sustainable”.

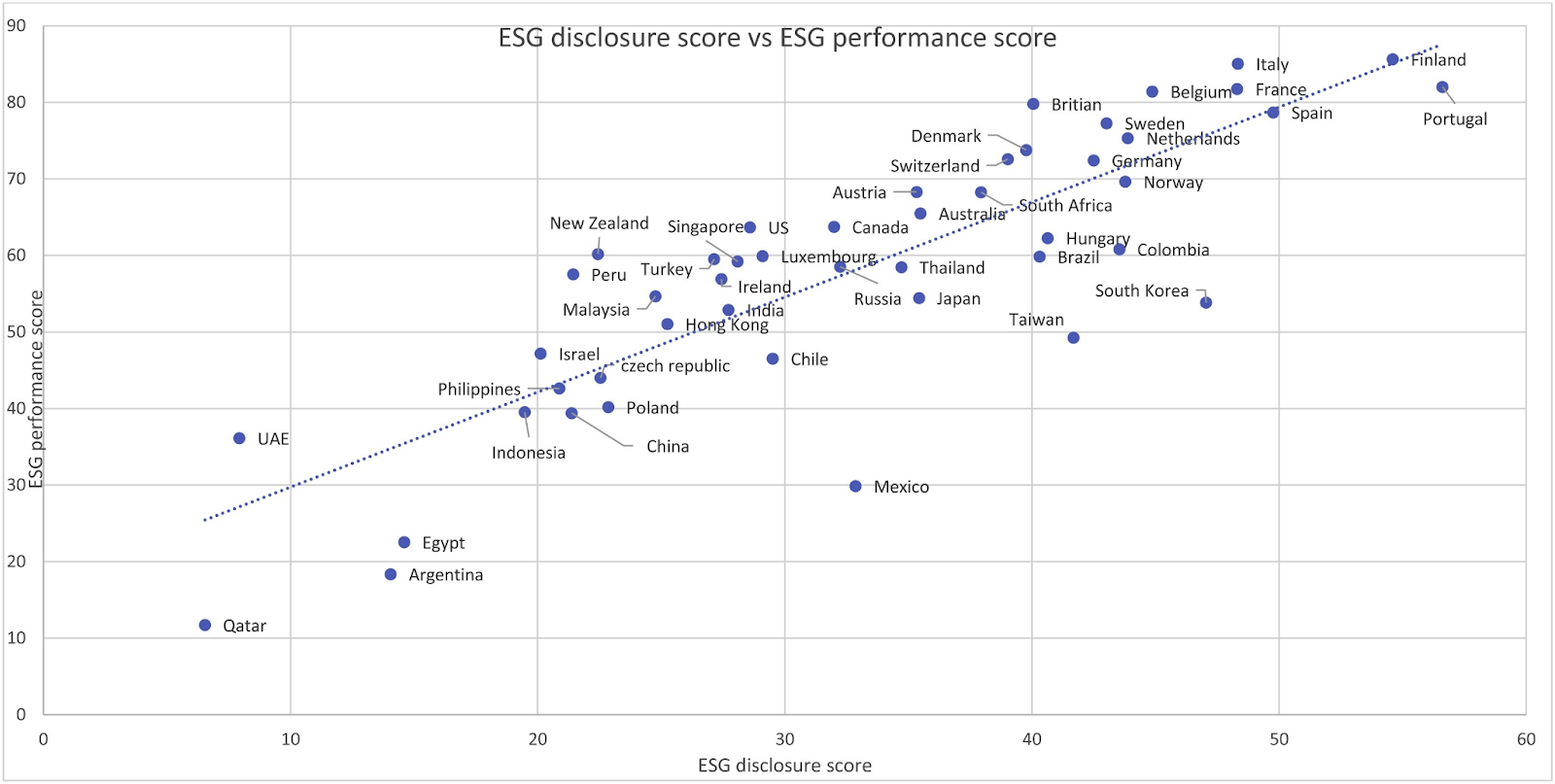

Yu et al. wrote a research article published in 2020 highlighting the presence and importance of greenwashing specific to environmental, social and governance disclosures. As defined by their study, greenwashing is when firms make misleading ESG disclosures; they disclose large quantities of ESG data but actually have poor ESG performance. Statistical results from Yu et al. showed that ESG performance scores are positively associated with ESG disclosure scores. Moreover, they found that peer-relative greenwashing scores were highly industry-dependent, with firms in the Materials industry having the highest peer-relative greenwashing score of 0.1522, followed by Energy (0.1477), and Utilities (0.1202).

Source: Yu et al. 2020

This study highlights the importance of understanding greenwashing as stakeholder demands for ESG increase. They highlight the current challenges of ESG disclosure, including the lack of standardization in disclosure rules of ESG data and global governing body to ensure the accuracy of reported ESG information, as well as the need to align ESG transparency with performance since greenwashing could become a barrier for investors who try to use ESG data in their investment strategy. (Yu et al 2020)

A Canadian Example: Royal Bank of Canada (RBC)

In October 2022, an inquiry was opened by the Competition Bureau regarding the Royal Bank of Canada (RBC) due to several accusations of greenwashing their investments. The allegations against them “suggest the bank has been marketing itself as being aligned with the climate goals of the Paris Agreement, all while continuing to finance the fossil fuel industry.” (Bernstein 2022) According to a fossil fuel finance report generated by a group of environmental organizations, RBC stands at fifth globally of banks funding the petroleum industry. On the other hand, RBC states in their climate blueprint that they are "fully committed" to supporting drastically reducing greenhouse gas emissions to net zero by 2050, including strategies like sustainable financing.

Judy Wilson, one of six entities who filed against RBC, is the chief of the Skat'sin te Secwepemc-Neskonlith Indian Band and the secretary-treasurer for the Union of British Columbia Indian Chiefs (UBCIC). As climate change brings a multitude of social issues pinned under the overhead environmental issue, environmentalists and communities affected by climate change like Wilson are taking action.

In recent times, regulators are also cracking down on businesses for greenwashing, as Keurig had just been fined in January 2022 for misleading consumers into believing that coffee pods could be recycled. This example further underlines the issue surrounding the lack of standardization in disclosure rules of ESG data or a global governing body to ensure the accuracy of reported ESG information.

What could remedy the issues surrounding greenwashing?

Although the lack of standardization is an issue occurring globally, it is currently in the process of being fixed. As mentioned previously, the CSA, SEC and ISSB all released proposals these past two years concerning climate-related disclosures, with all 3 referencing the TCFD framework and the GHG Protocol. The three organizations are making an effort to align in their disclosure requirements and standardizing key elements of the information and metrics required. The introduction of the CSSB and IRCSS into Canada to work with the ISSB to develop and support the adoption of their disclosure standards as well as the creation of independent Canadian standards signals the government’s commitment to alignment and to improving the reporting framework. This can lead to increased comparability between companies for investors, as well as decreased greenwashing. After all, the incoming mandatory disclosures as well as regulations impose restrictions and guidelines on how entities can report their ESG. The recent crackdown on greenwashing also sets the tone in the Canadian market on the regulators’ attitude towards such behavior and discouraging such actions.

Further recommendations proposed by Yu et al. propose reducing greenwashing behaviour through:

- Independent directors

- Institutional investors

- Influential public interests via a less corrupt country system

- Being cross-listed

Independent Directors and Institutional Investors

Prior studies of Corporate Social Responsibility (CSR) literature suggest that increased scrutiny from relevant stakeholders can have a direct effect on a firm’s greenwashing behavior. Yu et al’s empirical findings support this by suggesting that increased institutional ownership as well as a higher share of independent directors can reduce firms’ greenwashing behavior. After all, they believe this may be due to a firm’s unlikely engagement in ESG greenwashing “when relevant stakeholders exert greater scrutiny over the relationship between a company’s ESG performance and its ESG transparency.” (Yu et al 2020).

Influential public interests via a less corrupt country system

Yu et al's results demonstrate that a 1% increase in the factor of the absence of corruption leads to 0.60% less greenwashing. This means that citizens of a less-corrupt country may scrutinize firms’ greenwashing behavior and force them to address the issue, which could lead to less greenwashing overall.

Cross-listed companies

As said by Yu et al, prerequisites for cross-listing (listing stock in one or more foreign exchanges) by firms demands them to meet stricter disclosure requirements, which tend to lessen information asymmetry. Coupled with the scrutiny by foreign investors and stricter disclosure requirements, firms can be more discouraged from greenwashing.

These conclusions were reached based on their modelling of a dataset of 1925 companies from around the globe. The model examines whether firm-level features, country-level characteristics, and cross-listing status can discourage firms from engaging in greenwashing and examines the cross-country variation to specify the impacts of such elements on greenwashing behavior. (Yu et al 2020)

Concluding thoughts

The ESG reporting environment in Canada and worldwide is constantly evolving as government entities and boards scramble to adapt to the changing world as we know it. Although ESG reports are currently of little use to investors, that may change as new proposals and guidelines are released. The world is not only coming together to form an ESG reporting standard, but also uniting to make a difference in the environment by committing to reducing their carbon footprints and turning towards sustainable investing, financing and manufacturing. The rise in ESG also creates accountability for firms; as a consequence, communities are seeing real change happening before their eyes, whether it be planting trees or improved working conditions.

ESG as we know it is not only limited to stakeholder transparency and reducing risks for corporations and investors alike, but also making a material impact on the world’s climate. Tangible effects of the many steps forward we’ve taken in 2022, however, remains to be seen in the years to come. The only thing we can do now is to keep organizations accountable, and keep moving forward on our path to a greener world.

Written by: Michelle Lu

References

Alberta Securities Commission. (2022, October 12). CANADIAN SECURITIES REGULATORS CONSIDER IMPACT OF INTERNATIONAL DEVELOPMENTS ON PROPOSED CLIMATE-RELATED DISCLOSURE RULE. ASC. Retrieved from https://www.asc.ca/en/news-and-publications/news-releases/2022/10/12---csa-consider-impact-of-international-developments-on-proposed-climate-related-disclosure-rule

Amir Amel-Zadeh & George Serafeim (2018) Why and How Investors Use ESG Information:Evidence from a Global Survey, Financial Analysts Journal, 74:3, 87-103, DOI:10.2469/faj.v74.n3.2

Bains, R. S. (2021, October 25). CSA propose standardized and reinforced climate-related disclosure - primer on proposed National Instrument Ni 51-107 disclosure of climate-related matters. McMillan LLP. Retrieved from https://mcmillan.ca/insights/csa-propose-standardized-and-reinforced-climate-related-disclosure-primer-on-proposed-national-instrument-ni-51-107-disclosure-of-climate-related-matters/

Bernstein, J. (2022, October 16). Why environmentalists went after Canada's biggest bank for alleged greenwashing | CBC news. CBCnews. Retrieved from https://www.cbc.ca/news/science/rbc-greenwashing-investigation-1.6617129

Canadian National Railway Company. (n.d.). EcoConnexions programs. CN. Retrieved from https://www.cn.ca/en/delivering responsibly/environment/ecoconnexions-programs

Canadian National Railway Company. (n.d.). 2020 Sustainability Report. CN. Retrieved from https://www.cn.ca/en/delivering-responsibly/

Canadian Securities Administrators. (2021, October 18). Climate-Related Disclosure Update and CSA notice and Request For Comment . Canadian Securities Administrators. Retrieved from https://www.osc.ca/en/securities-law/instruments-rules-policies/5/51-107/51-107-consultation-climate-related-disclosure-update-and-csa-notice-and-request-comment-proposed.

Christensen, George Serafeim, Anywhere Sikochi; Why is Corporate Virtue in the Eye of The Beholder? The Case of ESG Ratings. The Accounting Review 1 January 2022; 97 (1): 147–175. https://doi.org/10.2308/TAR-2019-0506

Courtnell, J. (2023, February 10). ESG Reporting Preparation Guide: What is ESG reporting? Green Business Bureau. Retrieved from https://greenbusinessbureau.com/business-function/finance-accounting/esg-reporting-what-is-esg-reporting/

CPA Canada. (n.d.). An introduction to IFRS sustainability disclosure standards. CPA Canada. Retrieved from https://www.cpacanada.ca/en/business-and-accounting-resources/financial-and-non-financial-reporting/sustainability-environmental-and-social-reporting/publications/introduction-ifrs-sustainability-disclosure-standards

Deloitte. (n.d.). What is the TCFD and why does it matter? Deloitte. Retrieved from https://www2.deloitte.com/ch/en/pages/risk/articles/tcfd-and-why-does-it-matter.html

Deutsche Bank Wealth Management. (2019, November). CIO Special: The “S” in ESG: the ugly duckling of investing. Deutsche Wealth. Retrieved from https://www.deutschewealth.com/content/dam/deutschewealth/cio-perspectives/cio-special-assets/esg-investment-performance-challenges/CIO-Special-ESG-and-investment-performance-challenges-ahead.pdf

Ferrer, M. de. (2020, October 20). What is greenwashing and why is it a problem? euronews. Retrieved from https://www.euronews.com/green/2020/09/09/what-is-greenwashing-and-why-is-it-a-problem

Government of Canada. (2022, July 19). Climate Risk Management. Office of theSuperintendent of Financial Institutions. Retrieved from https://www.osfi-bsif.gc.ca/Eng/fi-if/rg-ro/gdn-ort/gl-ld/Pages/b15-dft.aspx#ann2.1

Gaia Melloni, Ariela Caglio, Paolo Perego. Saying more with less? Disclosure conciseness, completeness and balance in Integrated Reports, Journal of Accounting and Public Policy, Volume 36, Issue 3, 2017, ISSN 0278-4254,

https://doi.org/10.1016/j.jaccpubpol.2017.03.001.

Hsiao-Min Chen, Tsai-Chi Kuo, Ju-Long Chen. Impacts on the ESG and financial performances of companies in the manufacturing industry based on the climate change related Risks, Journal of Cleaner Production, Volume 380, Part 1, 2022, 134951, ISSN 0959-6526, https://doi.org/10.1016/j.jclepro.2022.134951.

IFRS. (2022, March). Exposure draft IFRS S2 climate-related disclosures. IFRS. Retrieved from https://www.ifrs.org/content/dam/ifrs/project/climate-related-disclosures/issb-exposure-draft-2022-2-climate-related-disclosures.pdf

IFRS. (2021, October 21). ISSB unanimously confirms Scope 3 GHG emissions disclosure requirements with strong application support, among key decisions. IFRS. Retrieved from https://www.ifrs.org/news-and-events/news/2022/10/issb-unanimously-confirms-scope-3-ghg-emissions-disclosure-requirements-with-strong-application-support-among-key-decisions/#1

Jonsdottir B, Sigurjonsson TO, Johannsdottir L, Wendt S. Barriers to Using ESG Data for Investment Decisions. Sustainability. 2022; 14(9):5157.

https://doi.org/10.3390/su14095157

Kotsantonis, S. and Serafeim, G. (2019), Four Things No One Will Tell You About ESG Data. Journal of Applied Corporate Finance, 31: 50-58. https://doi.org/10.1111/jacf.12346

KPMG LLP. (2021, November 21). ESG disclosure: Climate defense meets three lines of defense. KPMG. Retrieved from https://kpmg.com/ca/en/home/insights/2022/11/preparing-the-finance-function-for-esg-disclosures.html#:~:text=There%20are%20currently%20no%20legal,report%20it%20is%20largely%20voluntary.

Kroft, P. J., & Hamedani, G. (2022, August 30). Overview: OSFI's draft guideline B-15 on climate risk management. Miller Thomson LLP. Retrieved from https://www.millerthomson.com/en/publications/communiques-and-updates/financial-services-restructuring-communique/august-30-2022/overview-osfi-draft-guideline-climate-risk-management/

Michelson, Joan. (2022, November 18). ESG is ‘Soaring’. What does that mean? Forbes. Retrieved from https://www.forbes.com/sites/joanmichelson2/2022/11/18/esg-investing-is-soaring-what-does-it-mean/?sh=46abcc1351bc

PricewaterhouseCoopers. (2022, October 10). ESG-focused institutional investment seen soaring 84% to US$33.9 trillion in 2026, making up 21.5% of assets undermanagement: PWC Report. PwC. Retrieved from https://www.pwc.com/gx/en/news-room/press-releases/2022/awm-revolution-2022-report.html

Qiping Huang, Yongjia Li, Meimei Lin, Garrett A. McBrayer. Natural disasters, risk salience, and corporate ESG disclosure, Journal of Corporate Finance, Volume 72, 2022, 102152, ISSN 0929-1199, https://doi.org/10.1016/j.jcorpfin.2021.102152.

Redman, P. (2022, April 12). New TCFD ESG Disclosure Requirements in Canada and the UK. OneTrust. Retrieved from https://www.onetrust.com/blog/tcfd-esg-disclosure-requirements-canada-uk/

Securities and Exchange Commission. (n.d.). The Enhancement and Standardization of Climate-Related Disclosures for Investors. SEC.gov . Retrieved from https://www.sec.gov/rules/proposed/2022/33-11042.pdf

Simpson, S. (2021, November 1). Two thirds of Canadians (65%) consider ESG important factors when deciding on investment purchases. Ipsos. Retrieved from https://www.ipsos.com/en-ca/news-polls/two-thirds-of-canadians-consider-esg-important-factors-when-deciding-on-investment-purchases

Taylor, L. C. (2013, April 25). Joe Fresh customers vow boycott after Bangladesh factory collapse. Toronto Star. Retrieved from https://www.thestar.com/news/ world/2013/04/25/joe_fresh_customers_vow_boycott_after_bangladesh_factory_collapse.html?li_source=LI&li_medium=star_web_ymbii

Yu, Ellen Pei-yi; Bac Van Luu et al. Greenwashing in environmental, social and governance disclosures, Research in International Business and Finance, Volume 52, 2020, 101192. Retrieved from https://doi.org/10.1016/j.ribaf.2020.101192