Financial Inclusion: Designing Solutions to Provide Vital Economic Services

The Problem

Financial inclusion can be defined as non-discriminatory access to economic services- transactions, payments, savings, credit, and insurance – in a responsible and sustainable manner.[1]

Simply starting a bank account is often a gateway to broader prosperity. Moving away from cash reduces transaction costs, helps families and businesses plan long-term goals, and provides a mechanism for both financial and psychological security through services such as credit and insurance.[2]

However, despite these vast benefits, there are still an estimated 1.7 billion adults without a primary transaction account.[3]

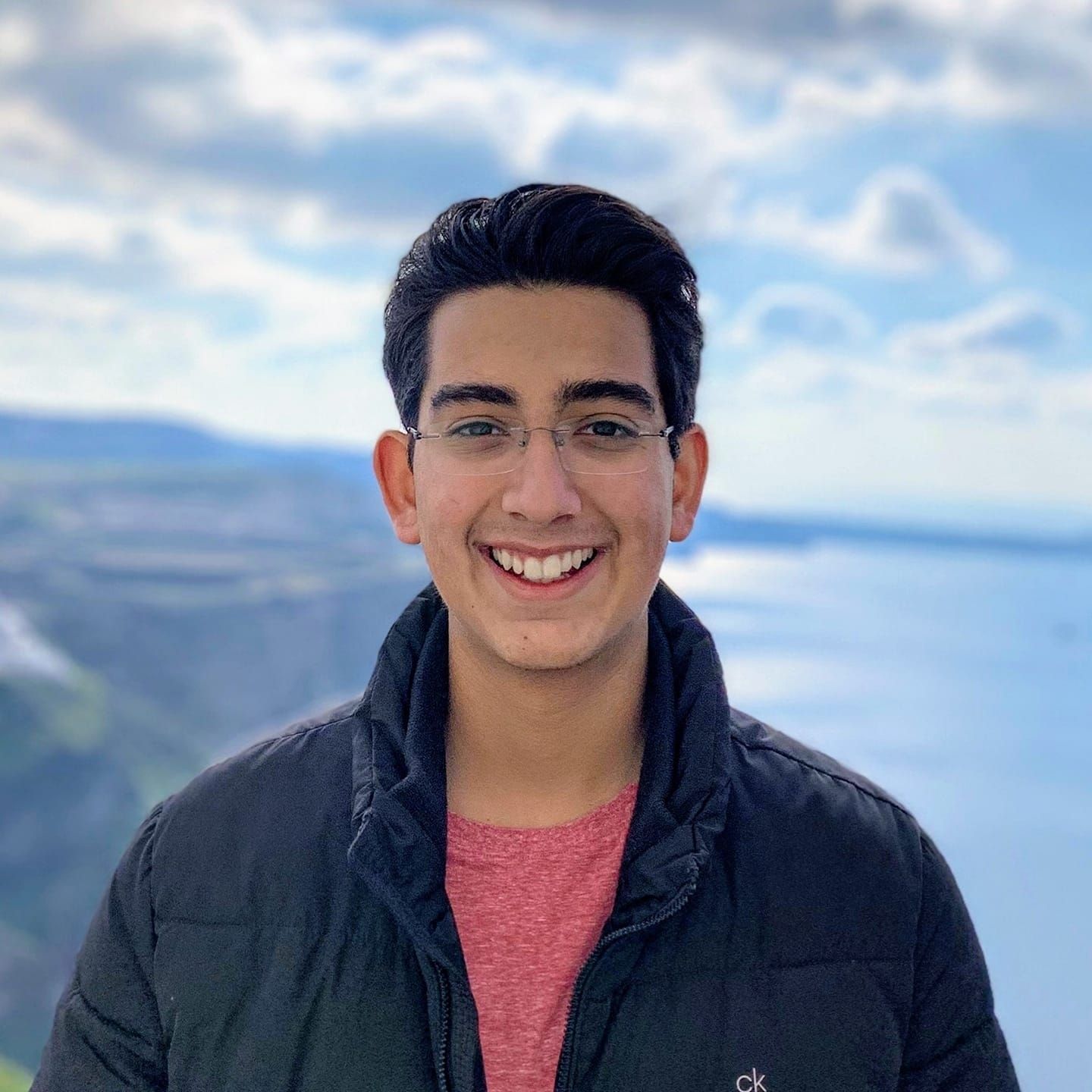

Step One: Understanding the Unbanked

Let us focus on this first step of opening accounts in financial institutions. A sizeable majority of the aforementioned 1.7 billion live in the developing world or emerging markets. On an average, 56% of unbanked adults, 980 million, are women. The percentage of men and women with access tends to drop as we go down the income ladder, regardless of the size of the broader economy. They are disproportionately young, and 62% of the unbanked did not have a primary education.[4]

Delving deeper, minimum deposit requirements were the most common barrier of entry with 20% of survey respondents citing this as their sole barrier. Interestingly, 30% did not have enough financial education to realize the need for an account often citing distrust in the financial system. Other significant barriers included excessive monetary and indirect administrative hassle-based costs especially in Latin America, distance to a bank branch and documentation required by banking agents in countries like Zambia, Philippines, and Zimbabwe.[5]

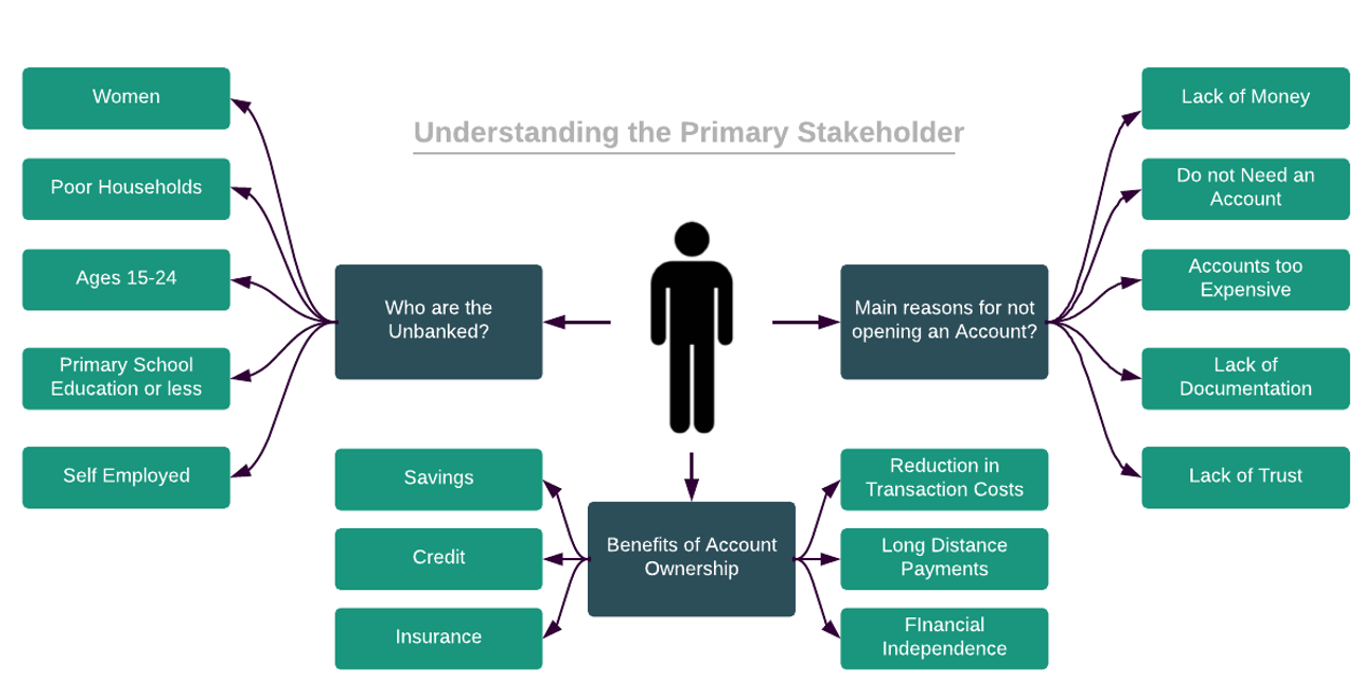

Step Two: Mapping the Solution Landscape

Human-centered design was pioneered by renowned the systems-engineer Michael Cooley.[6] It can be described as problem-solving that is deeply anchored to the need, contexts, and behaviors of the end user.[7] Embracing this philosophy, we repeatedly dive into the factors that inhibit individuals from accessing financial services until we arrive at the following solution landscape:

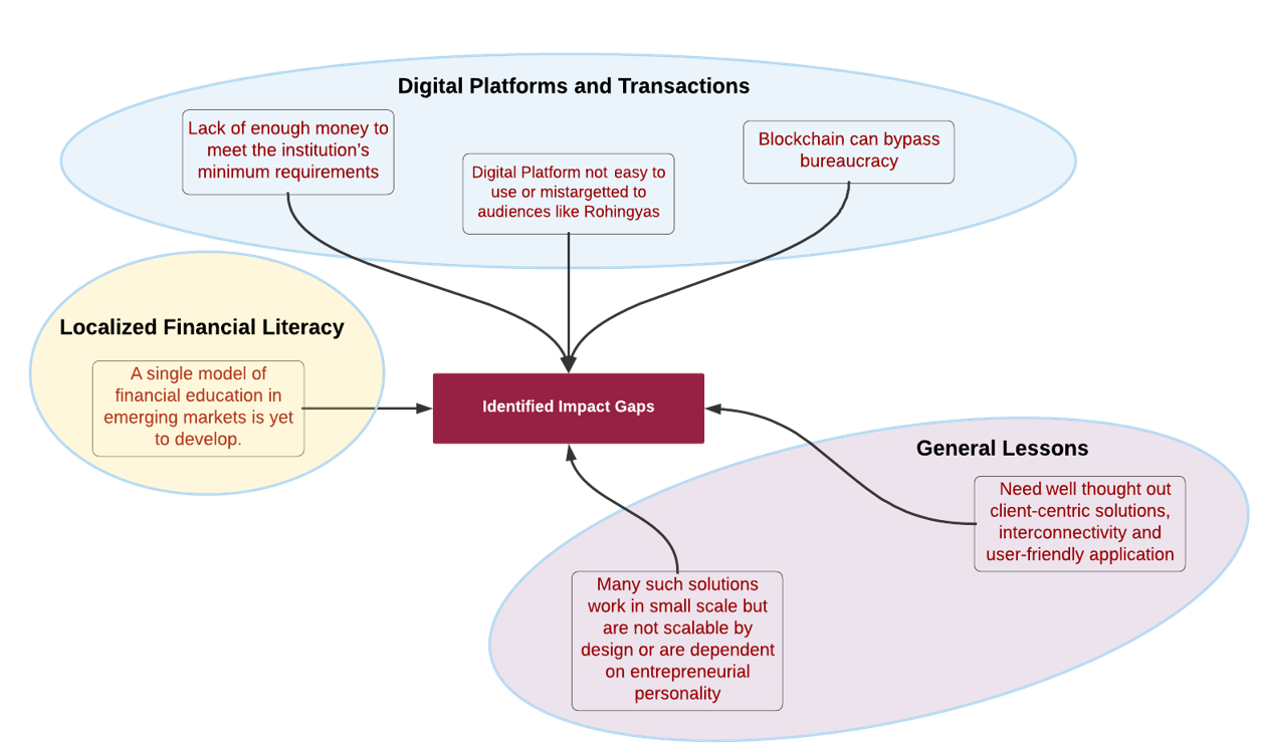

Step Three: Identifying Impact Gaps

Opportunity Sector I: Localized Financial Literacy

While direct impact solutions such as microfinance lending have received widespread attention, the first step of providing accounts is key to a more holistic solution. Now, this provision of accounts is not merely a question of distribution but of actively trying to financially educate and enable the users. Thus, the center for financial inclusion has expanded its definition of inclusion to recognize that everyone in the economy must be financially literate.

The center further noticed that a significant barrier to the growth of financial institutions is a lack of trust. Distrust breeds mainly due to governmental seizures of banks, history of economic discrimination, or past episodes of hyperinflation/bank runs. While nationalized personal finance education has its merits, a need for localized, region-specific, and user-centric financial literacy is ever-present. [8]

A lack of awareness pushes consumers out of the financial system; for example, farmers with a lower understanding of an insurance product are less likely to buy it. In that example, the research identified that peer effect plays a vital role in information transmission, and adoption efforts should tap into those local religious and economic communities.[9] Targeting high school students in Brazil improved student financial knowledge and empirically succeeding in improving their financial behavior well into adulthood.[10] Similarly, in Uganda, Grameen actively builds financial accountability among rural women through literacy initiatives and saving groups.[11]

Finally, there is tremendous room for innovation in the delivery channels used to reach the targeted audience. In one case, the use of a popular soap opera helped increased financial knowledge in South Africa.[12]

Opportunity Sector II: Digital Platforms and Transactions

Mobile Phones and the widespread adoption of the Internet in emerging markets have created financial transaction opportunities through novel methods. It is no surprise that financial institutions in urban settlements in emerging markets are moving from cost-intensive brick and mortar offices to mobile money. For example, M-Pesa, along with its domestic competitors, has provided 96% of Kenyan households access to formal financial services through text messaging and call-based transactions.[13] Moreover, ten years after M-Pesa’s launch, a study showed that a Kenyan family’s proximity to a mobile money agent was directly proportional to their likelihood of getting out of extreme poverty.[14]

According to the 2017 Gallup World Poll, 93% of adults in high income economies have access to a mobile phone while just 79% of adults have this luxury in developing economies[15]. In Bangladesh, Muhammad Yunus’ Grameen Bank has pioneered a “Telephone Ladies” system to bridge that digital divide.[16] Grameen helps rural women set up a village phone through which the local community can connect with their loved ones and access Grameen microfinance products.

Finally, biometric ID systems provide another way of lowering barriers to account ownership. A recent study conducted in Malawi and India suggested that biometric ID has enabled a rapid decline in unbanked adults and increased loan repayment rates.[17]

Conclusion

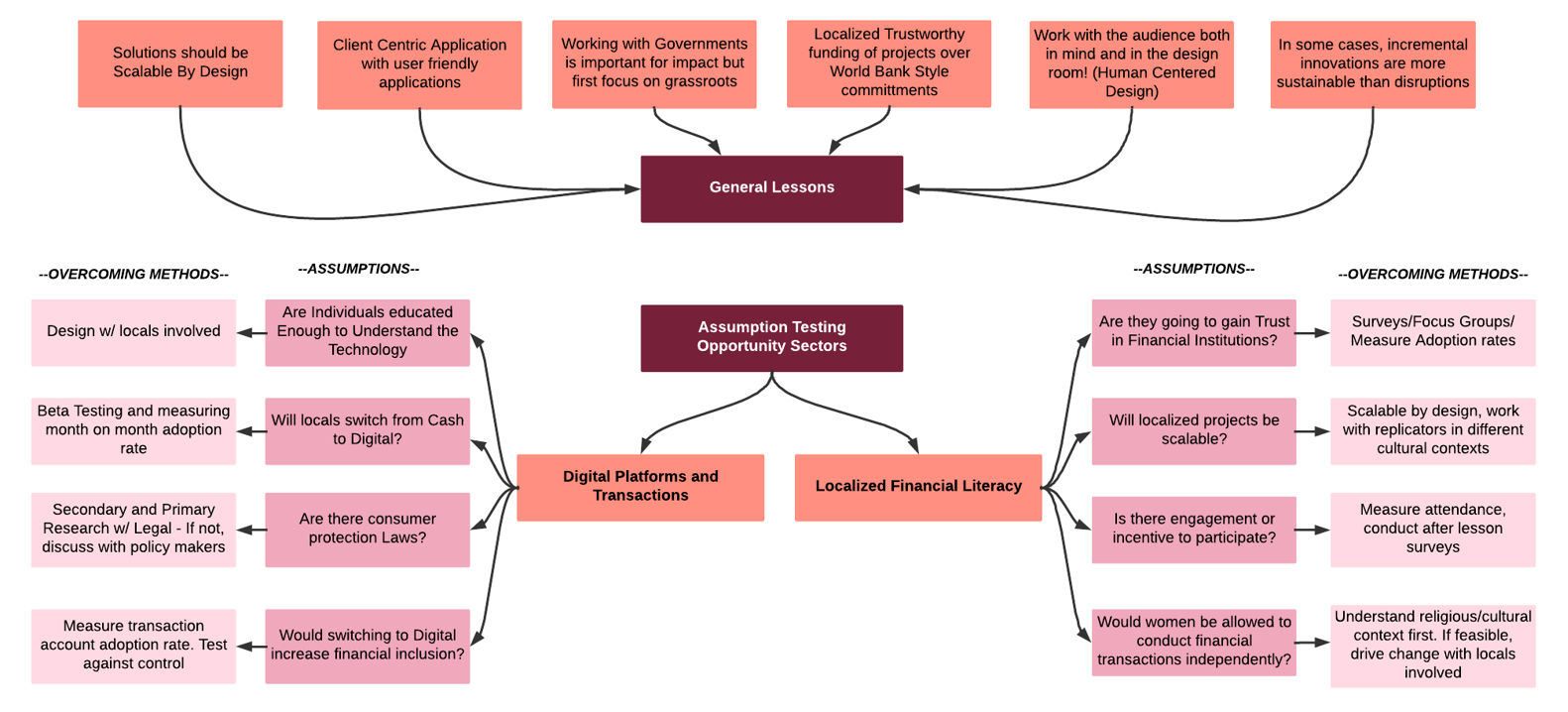

Financial literacy and digital transactions provide meaningful starting points for impact, however it is important to constant test our problem solving assumptions. For example developing a transaction app in regions with low literacy rate results in solutions that are overengineered and simply not effective. Often, by designing directly with locals involved or constantly testing the approaches, many such hurdles can be avoided.

By (1) defining the intention of innovation through carefully understanding the people affected, (2) brainstorming a set of solutions, and finally (3) realizing specific impact gaps, we have successfully identify opportunities and designed solutions to improve financial inclusion in emerging markets.

[1] https://www.worldbank.org/en/topic/financialinclusion/overview.

[2] https://www.theguardian.com/global-development-professionals-network/2014/oct/29/agricultural-insurance-smallholder-farmers-risk-financial-inclusion

[3] https://globalfindex.worldbank.org

[4] https://www.gatesfoundation.org/what-we-do/global-growth-and-opportunity/financial-services-for-the-poor

[5] https://www.gsma.com/mobilefordevelopment/wp-content/uploads/2012/06/fa2009_6.pdf

[6] https://link.springer.com/article/10.1007/s00146-016-0675-2

[7] https://www.designkit.org/human-centered-design

[8] https://www.imf.org/-/media/Files/Publications/WP/2020/English/wpiea2020157-print-pdf.ashx

[9] https://www.researchgate.net/publication/266336462_The_Economics_of_Agriculture_in_Africa_Notes_Toward_a_Research_Program

[10] https://www.researchgate.net/publication/309408485_The_Impact_of_High_School_Financial_Education_Evidence_from_a_Large-Scale_Evaluation_in_Brazil

[11] https://www.centerforfinancialinclusion.org/savings-groups-mobile-phones-and-a-new-solution-for-rural-women

[12] https://academic.oup.com/jeea/article-abstract/15/5/1025/2995881

[13] https://edition.cnn.com/2017/02/21/africa/mpesa-10th-anniversary/index.html

[14] https://www.jefftk.com/suri2016.pdf

[15] https://news.gallup.com/opinion/gallup/235151/mobile-tech-spurs-financial-inclusion-developing-nations.aspx

[16] http://news.bbc.co.uk/2/hi/south_asia/4471348.stm

[17] https://www.files.ethz.ch/isn/142885/1425165_file_Gelb_Decker_biometric_FINAL.pdf