Fintech and Social Impact: Financial Accessibility in the 21st Century

Applications of financial technology (fintech) can be seen everywhere in our day-to-day lives. Ranging from small transactions with Apple Pay to revolutionary creations such as blockchain, fintech is becoming instrumental in shaping the world we live in. Fintech is valuable for many reasons, but an often overlooked feature is its ethical significance. Fintech's accessibility is a powerful tool in an industry historically plagued with discrimination.

Why Traditional Banking Systems Simply Don’t Work

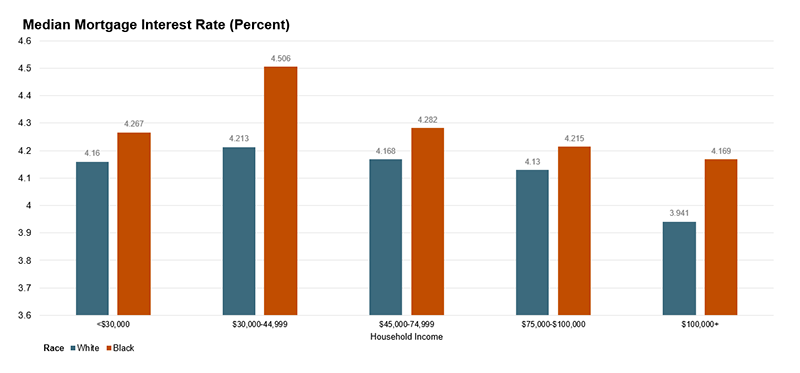

For many of us, banks are fantastic conveniences: they store our money safely, generate interest, and help us plan major financial decisions. For businesses, banks are necessary to conduct nearly all operations. However, for many marginalized groups, banks are the gates that perpetuate racial inequality. For the majority of people, especially those with little disposable income, home equity is their primary source of wealth accumulation (Boehm & Schlottmann, 2004). However, home mortgage lenders, especially majority banks, deny Black applicants at a rate 80% higher than white applicants (Home Mortgage Disclosure Act, 2020). Even for those approved, data from a 2019 housing survey conducted by the US Census Bureau show high income lack homeowners pay higher interest on mortgages than white homeowners in all income brackets.

Caption: Source: JCHS tabulations of U.S. Census Bureau data, 2019 American Housing Survey.

This issue isn't just limited to race: financial inclusion continues to remain a struggle in the developing world and rural areas in the developed world. According to the International Labor Office, about 70% of adults in the developing world have no access to financial services, despite many rural households having relatively stable and diverse sources of income. Without these services, it is difficult for households to accumulate wealth in face of inflation. In the developing world and low-income areas, financial services aren't just a convenience, but a lifeline.

Facilitating access to financial planning and services is a key step to reducing global poverty. Access to debt financing, for example, gives low-income families new opportunities to invest in their education and health, or start a business, boosting local economies and creating new sources of wealth in rural communities- areas especially susceptible to economic stagnation. Greater financial accessibility can open new doors to our most disadvantaged, resulting in greater economic stability and social mobility.

Fintech: A Modern Solution to Financial Accessibility

Here's where fintech comes in. Fintech services, especially online banking and digital payments, allows anyone to access financial services as long as they have a mobile phone with Internet access. Mobile apps such as Tangerine, Wealthsimple, TransferWise, and Paypal can be downloaded for free with the touch of a button and easily set up. These fintech companies offer both traditional and alternative banking services such as easy access to lines of credit and micro-investing tools, while being far more accessible for groups of people that struggle to access banks in person.

But wait! You can’t just assume everyone has a smartphone! What if somebody in poverty can’t afford a smartphone? Fortunately, we can. As of 2022, an estimated 83% of the world’s population owns a smartphone, allowing a safe assumption that most working-age adults have access to a smartphone.

The low requirements to access these services and large range of options make fintech apps a better alternative for minority groups that have had bad experiences with traditional banking systems, individuals who lack the time and/or resources to visit a bank, and inhabitants of rural areas. Through these services, people everywhere have a variety of choices for sending and receiving money, applying for loans, and building financial resiliency.

Even while fintech is still in its early stages of development, its impact is clear: a 2021 joint paper from Case Western Reserve University and the American Enterprise Institute found that fintech mortgage lenders show little to no gap in lending terms provided to Black and Hispanic borrowers after adjusting for GSE credit-risk pricing determinants and loan size. In 2019, Gobind Singh Deo, the Communications and Multimedia Minister in Malaysia, praised TransferWise, a fintech payment and currency conversion company, for its role in growing Malaysia's economy through remittances.

Conclusion

Fintech is proving to be a solution to alleviating wealth inequality and discrimination in traditional banking systems. It grants the opportunity for financial services to transcend geographical boundaries and wealth classes, increasing financial inclusion globally. As fintech solutions continue to grow and evolve, it is important to recognize its role in financial accessibility and social impact.

Sources:

https://www.huduser.gov/publications/pdf/wealthaccumulationandhomeownership.pdf

https://www.worldbank.org/en/topic/financialinclusion/overview

https://www.radicati.com/wp/wp-content/uploads/2021/Mobile_Statistics_Report,_2021-2025_Executive_Summary.pdf

Images: