Bridging Theoretical Ideals and Real-World Realities: Welfare Economics in the Pursuit of Balanced Societal Well-being

GRC 2023 Global Essay Competition Top 30

By Nicholas Li

“The term welfare economics refers to a general framework for normative analysis, that is, for evaluating different choices that society may make.” As Shavellc (2003) noted, societal welfare maximization occurs through a combination of hedonistic and communal utilities. This aligns with the fundamental economic maxim to allocate scarce resources with economic production, wealth distribution, and consumption of both the individual and collective in mind. Without ample consideration of these three factors, a misallocation of capital could pose significant challenges to the well-being of both current and future generations, as seen in the Soviet Union’s Collectivization in the early 20th century, the Venezuelan Economic Crisis in the 2010s, and China’s recent economic downturn due to an oversight in the distribution of government stimuli. To balance these aspects, welfare economics introduces a comprehensive approach that extends beyond individual preferences to encompass a broader societal context.

Often, economic models fail to accurately represent real-life circumstances as they face excess burdens from human nature to deviate from purely rational decision-making. One of the quintessential theories of overconsumption is the tragedy of the commons. When individuals act solely in pursuit of their self-interest without regard for the finite nature of shared resources, the result is depletion, degradation, and a compromised ability to meet the community’s needs (Ostrom, 2002).

Standard economic theory attributes such negative externalities to the failure of markets to internalize externalities and account for the broader social costs associated with resource allocation. To address these, welfare economics provides a framework that integrates ethical considerations into economic decision-making. The theory of social optimization is anchored in the First and Second Welfare Theorems, which delineate the conditions under which competitive markets lead to Pareto efficiency—a state where resources are allocated optimally and no individual can be better off without making someone else worse off. Coleman (1980) defined that “allocations that are Pareto superior increase at least one person’s utility without adversely affecting the utility of another; they produce winners but no losers.” In this sense, all economic policy created should be Pareto improvement.

Government interventions, such as Pigouvian taxes that aim to correct market failures by internalizing externalities, are crucial in aligning private incentives with societal well-being. Against the tragedy of commons situation, Pigouvian taxes are instrumental in internalizing the external costs associated with the overuse of common resources. Against the tragedy of the commons situation, Pigouvian taxes act as a deterrent, discouraging individuals from exploiting shared resources excessively for personal gain. By assigning a monetary value to the negative externalities generated by overconsumption, these taxes create a financial disincentive, steering behavior towards more sustainable and socially responsible practices.

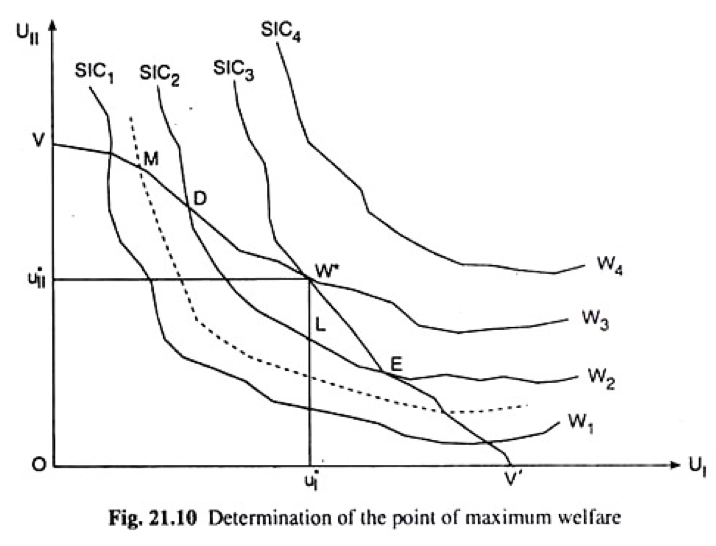

However, the real-world application of such interventions encounters issues vis-à-vis the intricacies of human behavior. The grand utility frontier (GUF) discerns the trade-offs inherent in resource allocation decisions, balancing a multitude of preferences against numerous others, creating a Pareto optimum, as shown in Figure 1. The model draws from the Edgeworth Box, where individual indifference curves are juxtaposed to represent potential allocations that maximize overall societal well-being. The GUF and the Edgeworth Box showcase the potential Pareto improvements achievable through thoughtful policy interventions. During the reunification of East and West Germany, as the two regions integrated their previously separated economies, economists utilized the two theories and others to model the trade-offs and potential Pareto improvements resulting from reallocating resources and wealth between the previously distinct systems. This application allowed policymakers to identify strategies to maximize societal well-being while minimizing disruptions.

Additionally, the three primary axioms—completeness, transitivity, and continuity—form the foundation of understanding individual choices. Although these models have been robust, preferences are dynamic, subject to cultural influences, and may not always conform to the assumptions of traditional economic models. This can be seen in the last decade’s surge in cryptocurrency markets. While traditional economic models assume rational decision-making based on preferences, the volatile nature of cryptocurrency investments illustrates a departure from the completeness, transitivity, and continuity axioms. Investors’ decisions are often influenced by psychological factors, market sentiments, and speculative trends, challenging the traditional understanding of revealed preferences. These issues pose significant hurdles in achieving a harmonious balance between economic growth, resource consumption, and wealth distribution, thereby emphasizing the ongoing need for nuanced analyses and innovative solutions in the pursuit of sustainable development.

Building off of models from prior writers, including Pigou, Pareto, and Lerner, modern applications demand an exploration of interdisciplinary perspectives, a recognition of the dynamic nature of preferences, and a commitment to refining models in response to real-world complexities. The ongoing need for innovative solutions remains central to the pursuit of sustainable development, and by embracing the evolving landscape of economic behaviors and preferences, economists can contribute to a more comprehensive understanding of societal welfare and pave the way for pragmatic policies that address the intricacies of the contemporary world.

Figure 1: Social Welfare Maximization, Credit: Lawrence Leung

Figure 2: Edgeworth Box, Credit: Vanshika Gho